US Treasury Yield Curve

The yield curve plots US Treasury yields across maturities (1 month to 30 years). When short-term yields rise above long-term yields — an inversion — it has historically preceded recessions. Data from the St. Louis Fed (FRED), refreshed daily.

10Y−2Y spread: +0.27% — last inversion ended August 27, 2024 after 537 trading days.

Yields by maturity

| Maturity | Today | 1 month ago | 1 year ago |

|---|---|---|---|

| 1M | 3.68% | 3.72% | 4.20% |

| 3M | 3.83% | 3.68% | 4.39% |

| 6M | 3.91% | 3.78% | 4.29% |

| 1Y | 3.98% | 3.83% | 4.07% |

| 2Y | 4.20% | 4.08% | 3.90% |

| 5Y | 4.27% | 4.25% | 3.96% |

| 7Y | 4.37% | 4.41% | 4.16% |

| 10Y | 4.49% | 4.57% | 4.38% |

| 20Y | 4.95% | 5.09% | 4.90% |

| 30Y | 4.93% | 5.10% | 4.89% |

10Y–2Y inversions in our data (since 2001)

| Began | Ended | Trading days | Deepest |

|---|---|---|---|

| July 6, 2022 | August 27, 2024 | 537 | -1.08% |

| May 30, 2007 | June 6, 2007 | 5 | -0.04% |

| May 3, 2007 | May 22, 2007 | 13 | -0.06% |

| August 17, 2006 | March 21, 2007 | 147 | -0.19% |

| June 30, 2006 | July 27, 2006 | 18 | -0.07% |

| June 8, 2006 | June 29, 2006 | 15 | -0.06% |

| March 21, 2006 | March 30, 2006 | 7 | -0.05% |

| January 31, 2006 | March 8, 2006 | 25 | -0.16% |

Episodes of 5+ consecutive trading days below zero.

Methodology & sources

Yields are constant-maturity US Treasury rates published by the Federal Reserve (FRED series DGS1MO–DGS30); the spread is FRED's T10Y2Y (10-year minus 2-year). An "inversion" here means the 10Y–2Y spread closed below zero. Our data begins in 2001, so earlier inversions (e.g. 1989, 2000) are not listed. Updated twice daily. See the broader Market Valuation & Macro dashboard for rates, inflation, volatility, and more.

Source: U.S. Federal Reserve (FRED). For informational purposes only; not investment advice.

FAQ

- What is the US Treasury yield curve?

- The yield curve plots US Treasury yields across maturities, from 1 month to 30 years. Its shape reflects the market's expectations for growth and interest rates — normally longer maturities pay more than shorter ones.

- Is the yield curve inverted right now?

- As of June 18, 2026, the 10-year minus 2-year Treasury spread is +0.27%, so the yield curve is not inverted.

- Why does an inverted yield curve matter?

- The curve inverts when short-term yields rise above long-term yields. Historically, a sustained 10Y–2Y inversion has preceded every US recession in recent decades, which is why it's watched closely as a recession warning — though the lead time varies.

More visualizations

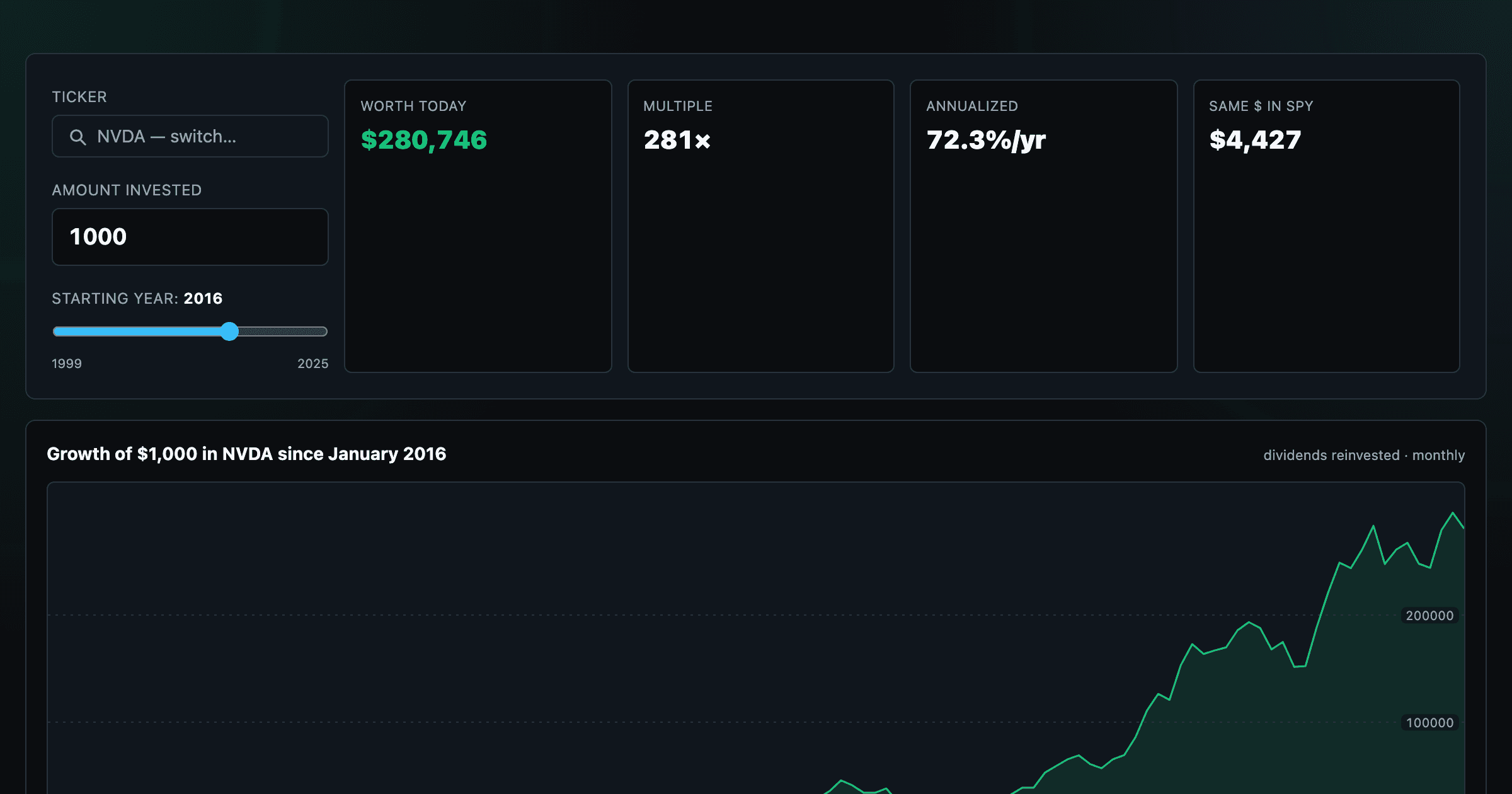

What $1,000 in any stock or ETF would be worth today.

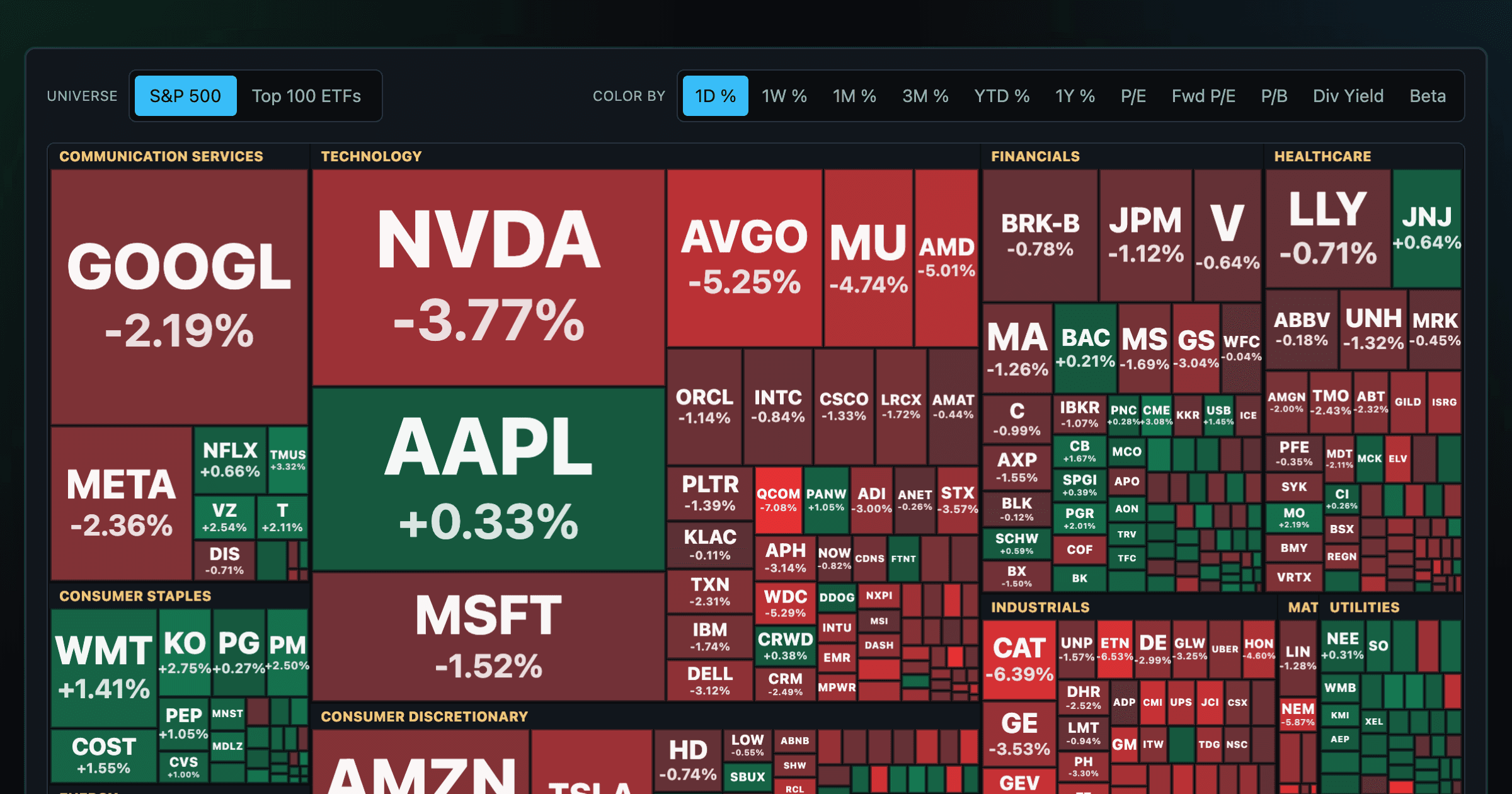

Every S&P 500 company sized by market cap — color by return or valuation.

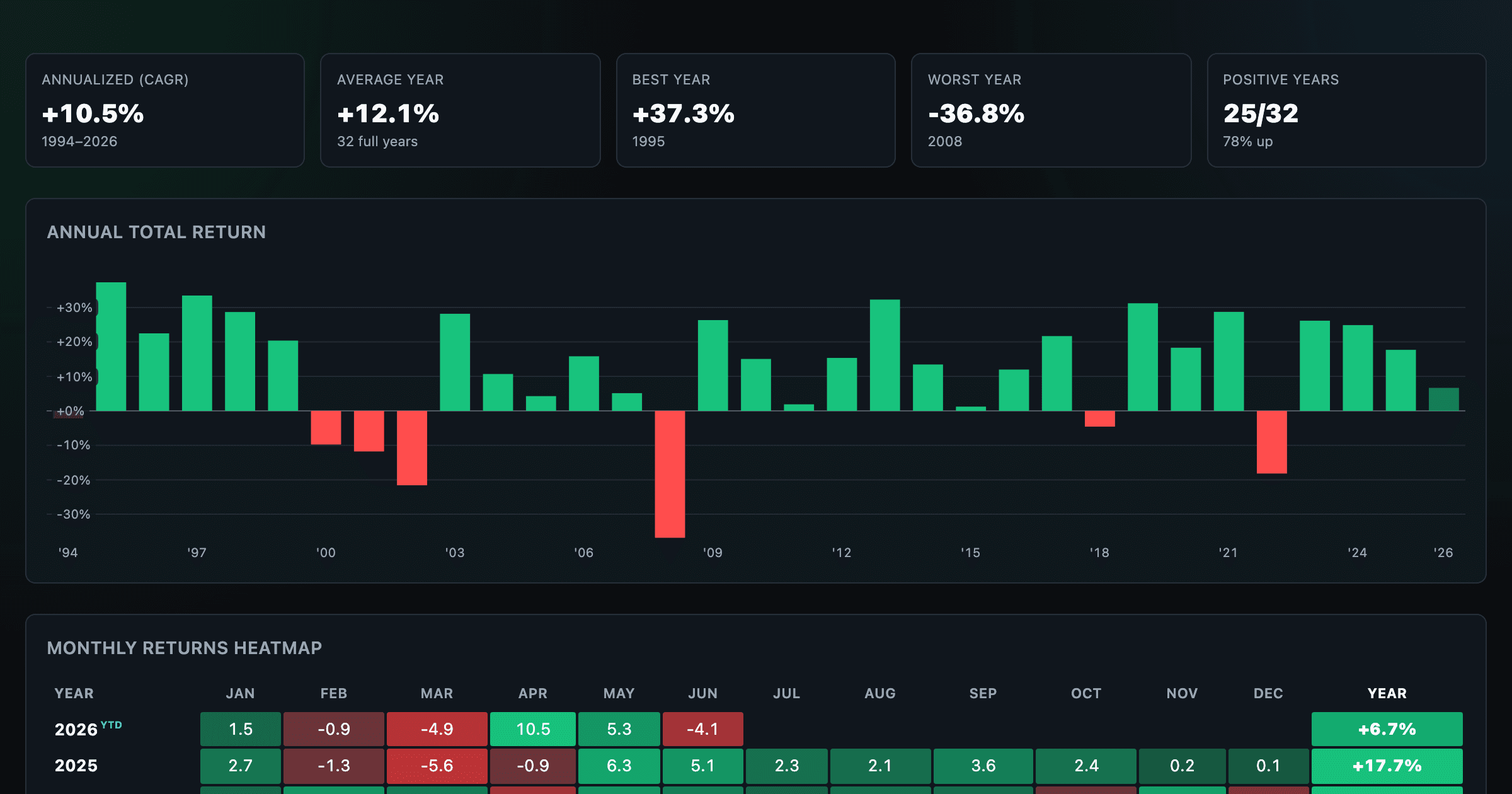

S&P 500 annual and monthly returns — every year, every month.

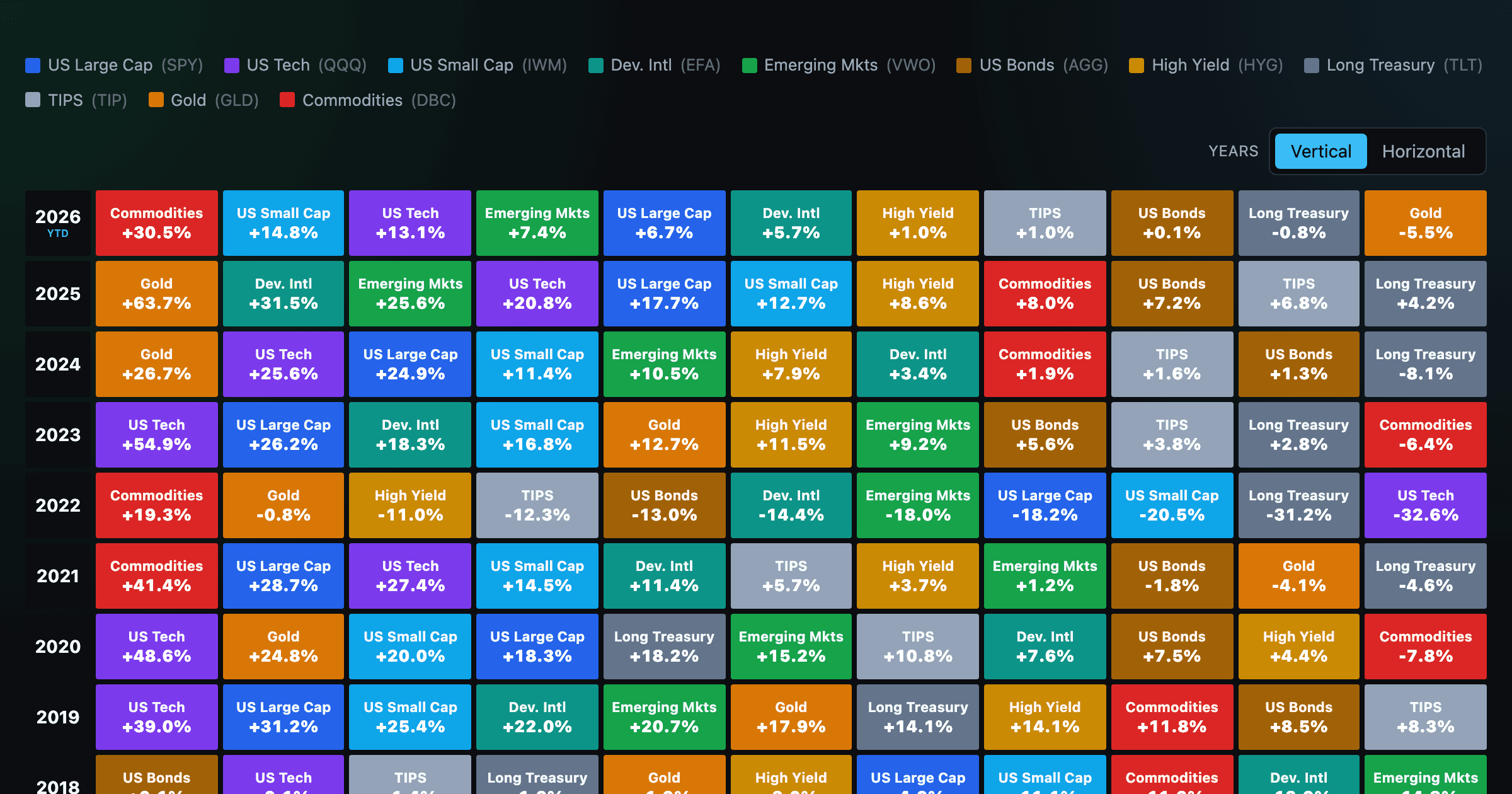

Asset-class returns ranked year by year — the Callan chart / asset allocation quilt.

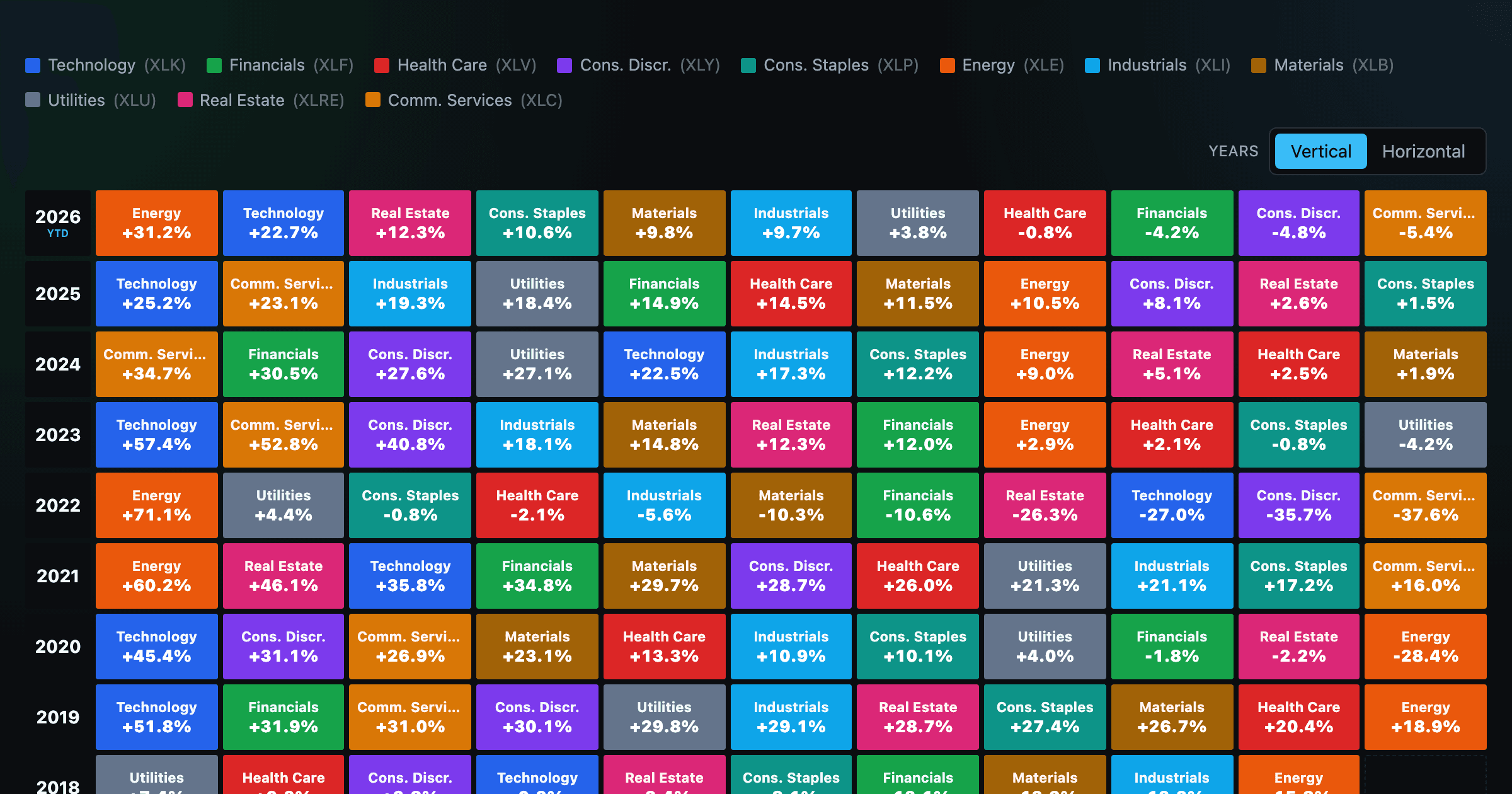

The 11 S&P 500 sectors ranked year by year — a sector quilt chart, back to 1999.

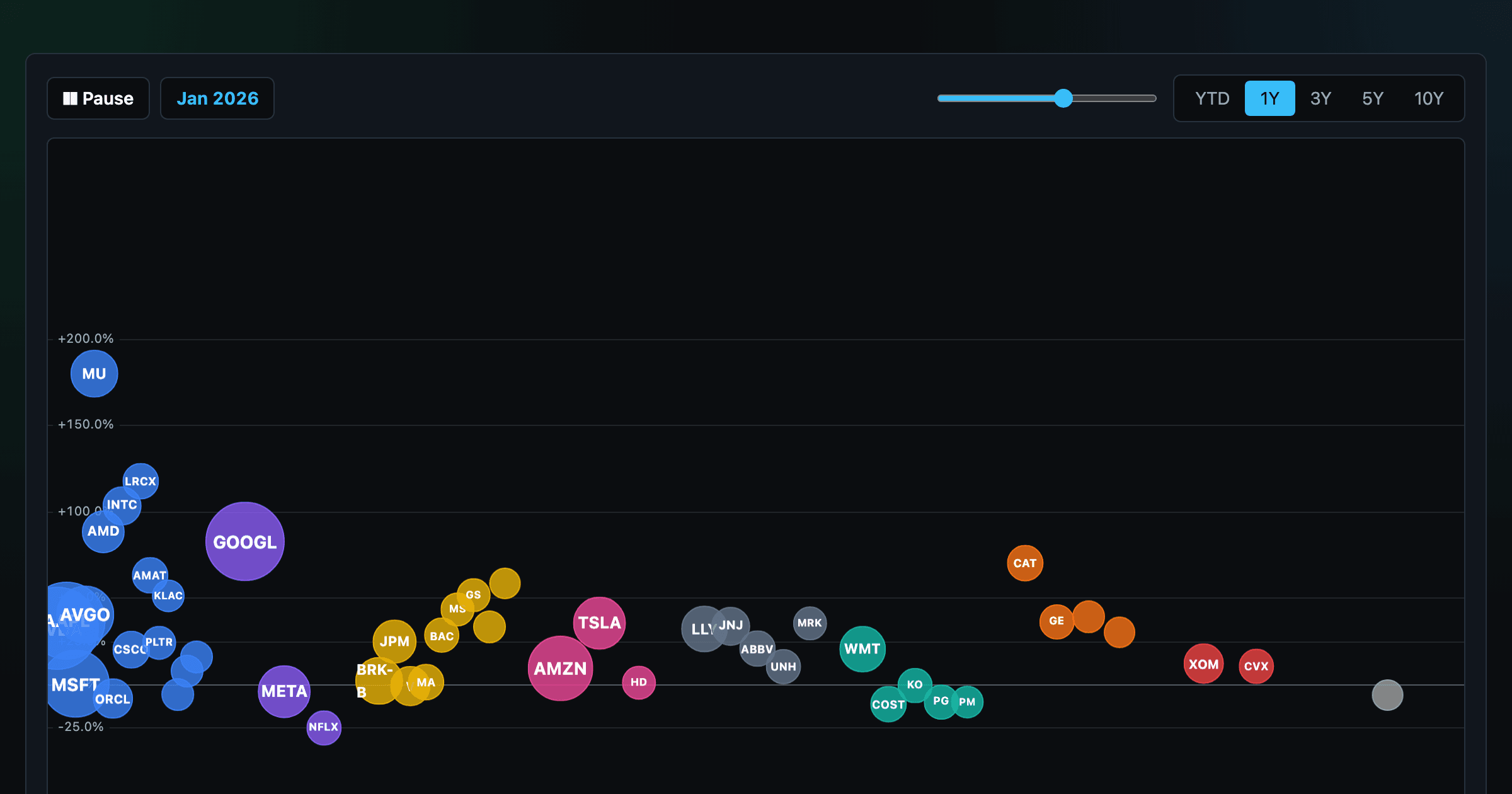

The biggest US companies as animated bubbles, rising and falling with their total return over time.

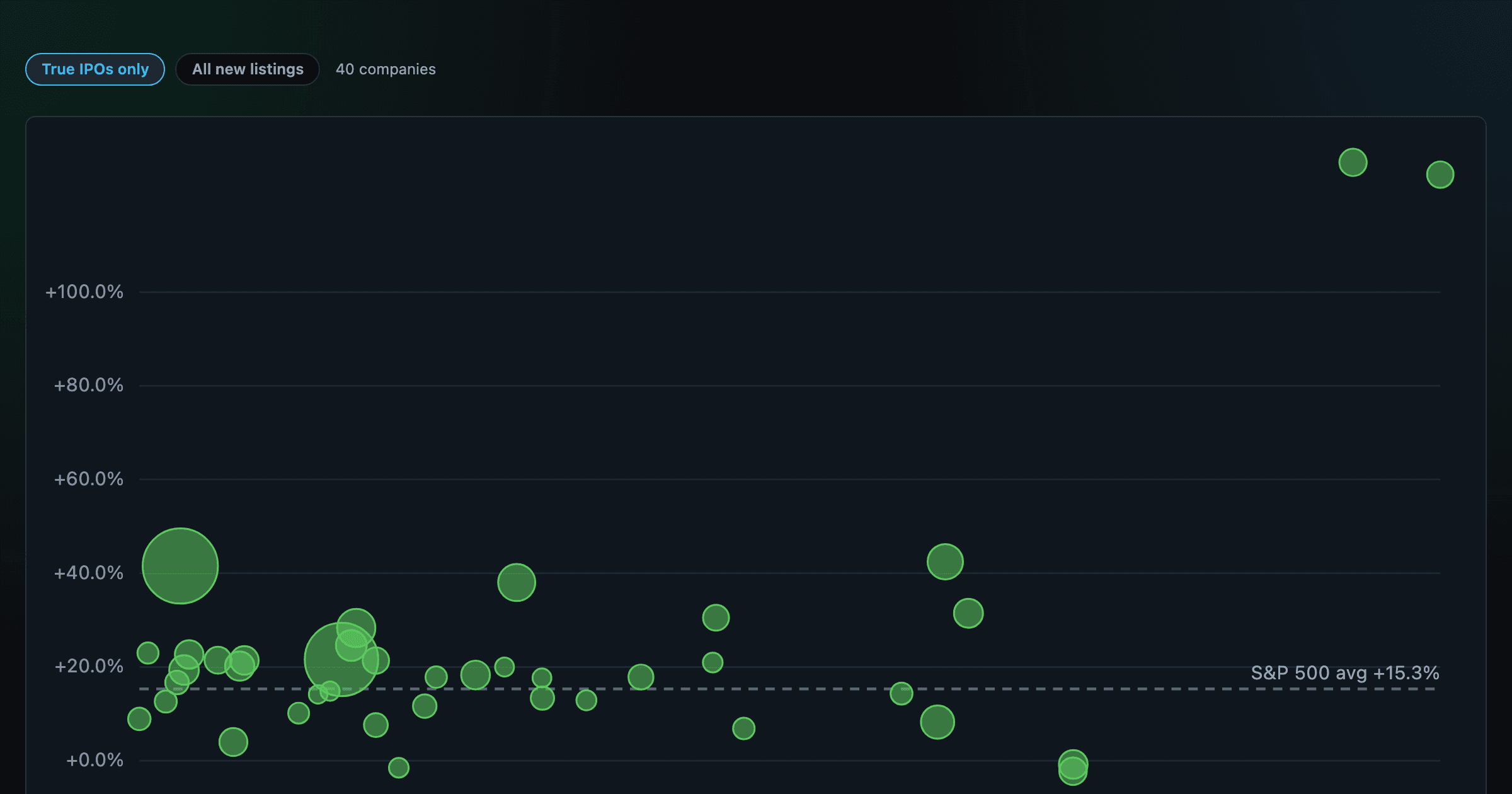

How recent stock-market debuts have performed since listing — annualized, vs the S&P 500, by IPO vs spin-off.

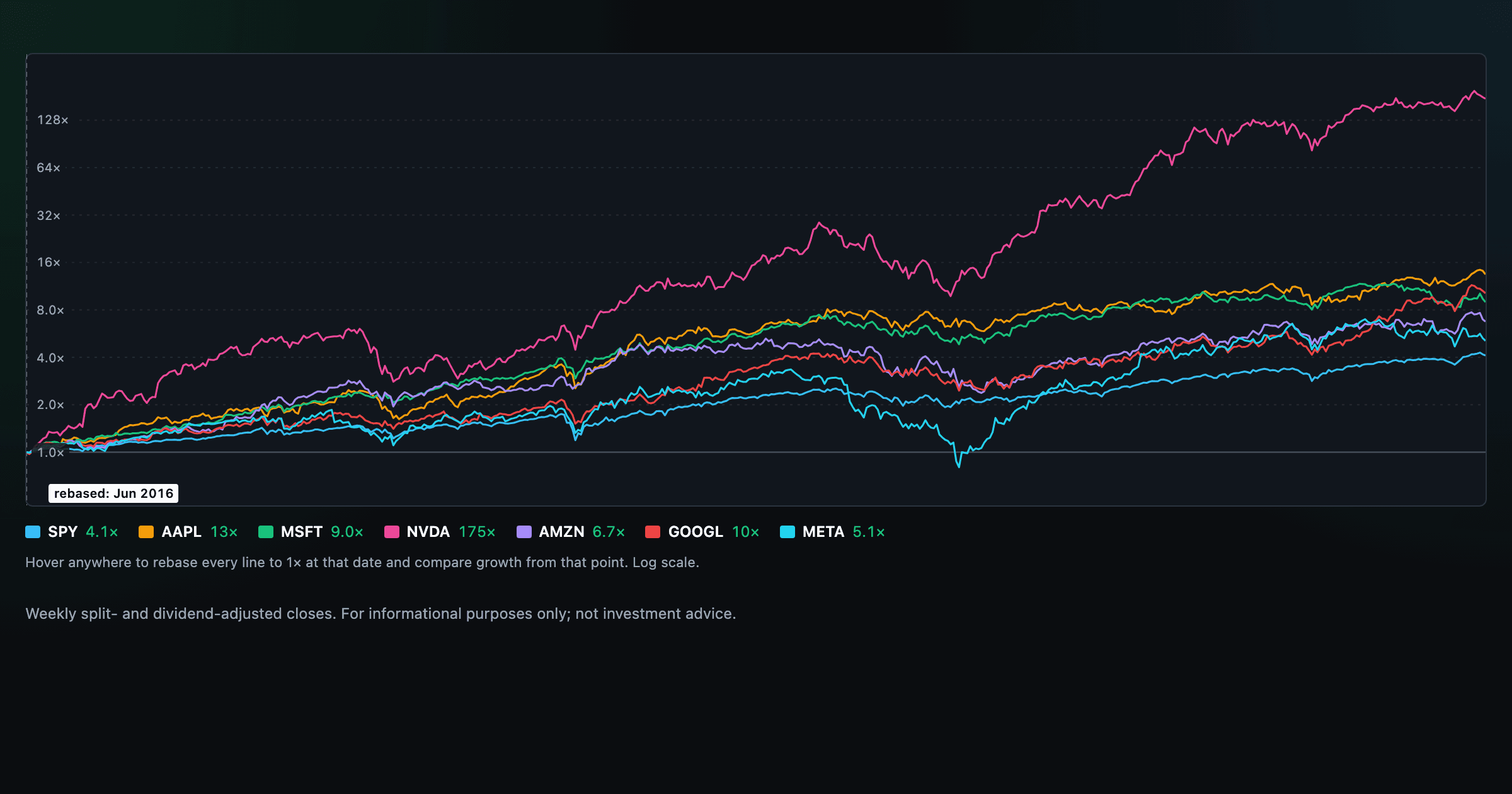

Compare megacaps vs the S&P 500, rebased to 1× at any date you hover.

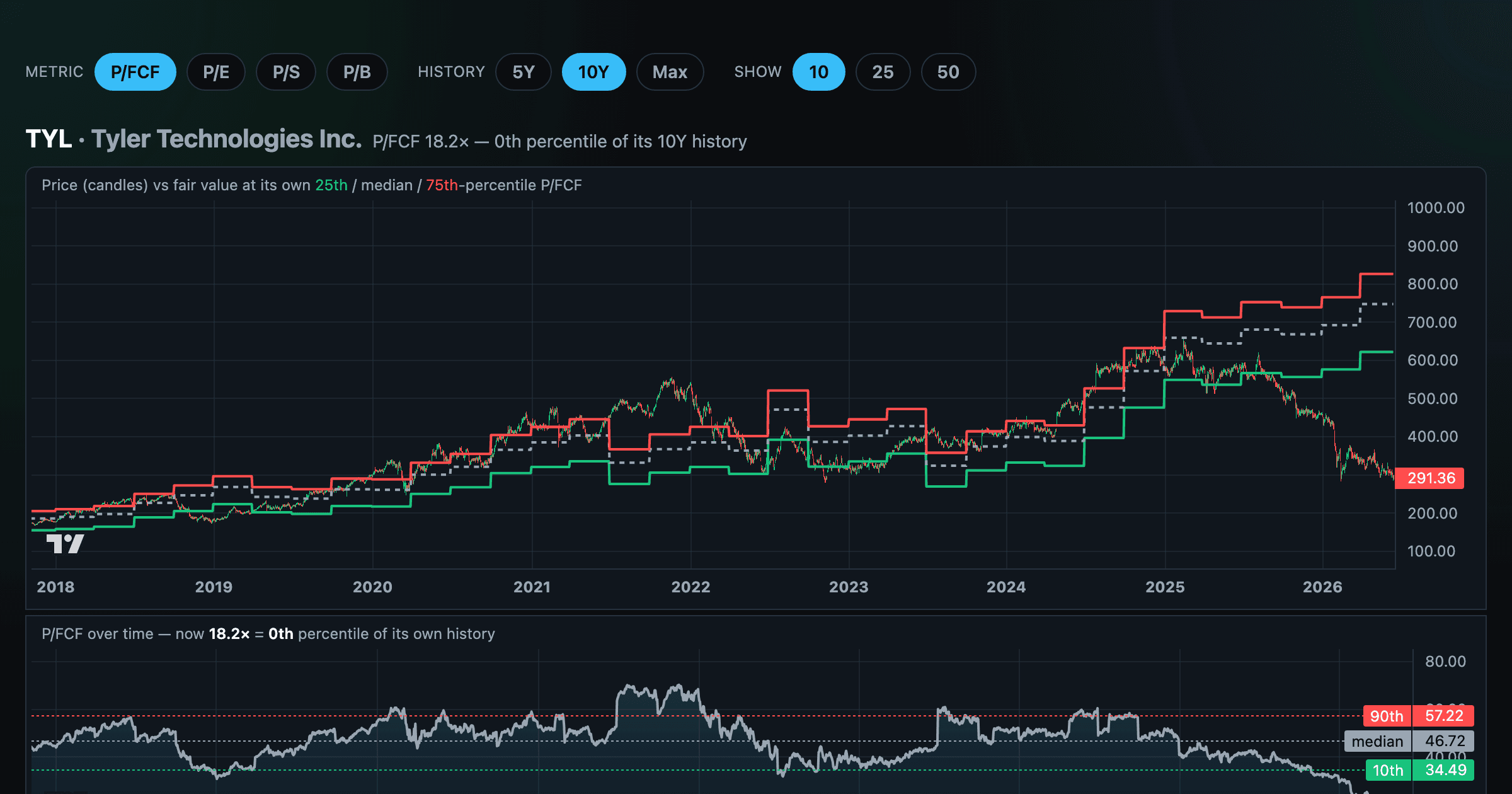

Stocks trading cheapest relative to their own P/E, P/FCF, P/S, or P/B history — with fair-value bands.

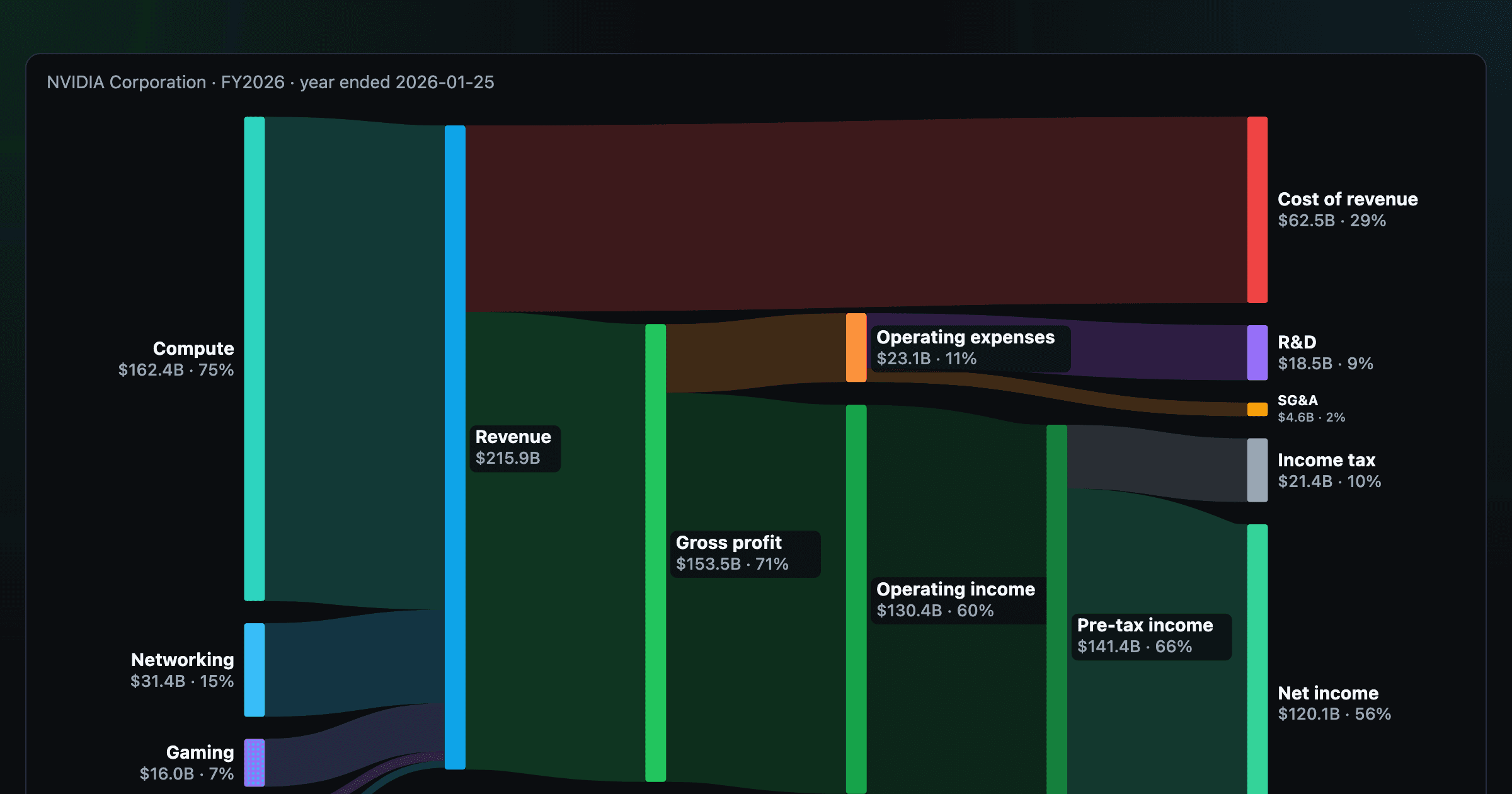

Follow a company's revenue through its income statement as a Sankey — costs, taxes, and profit.

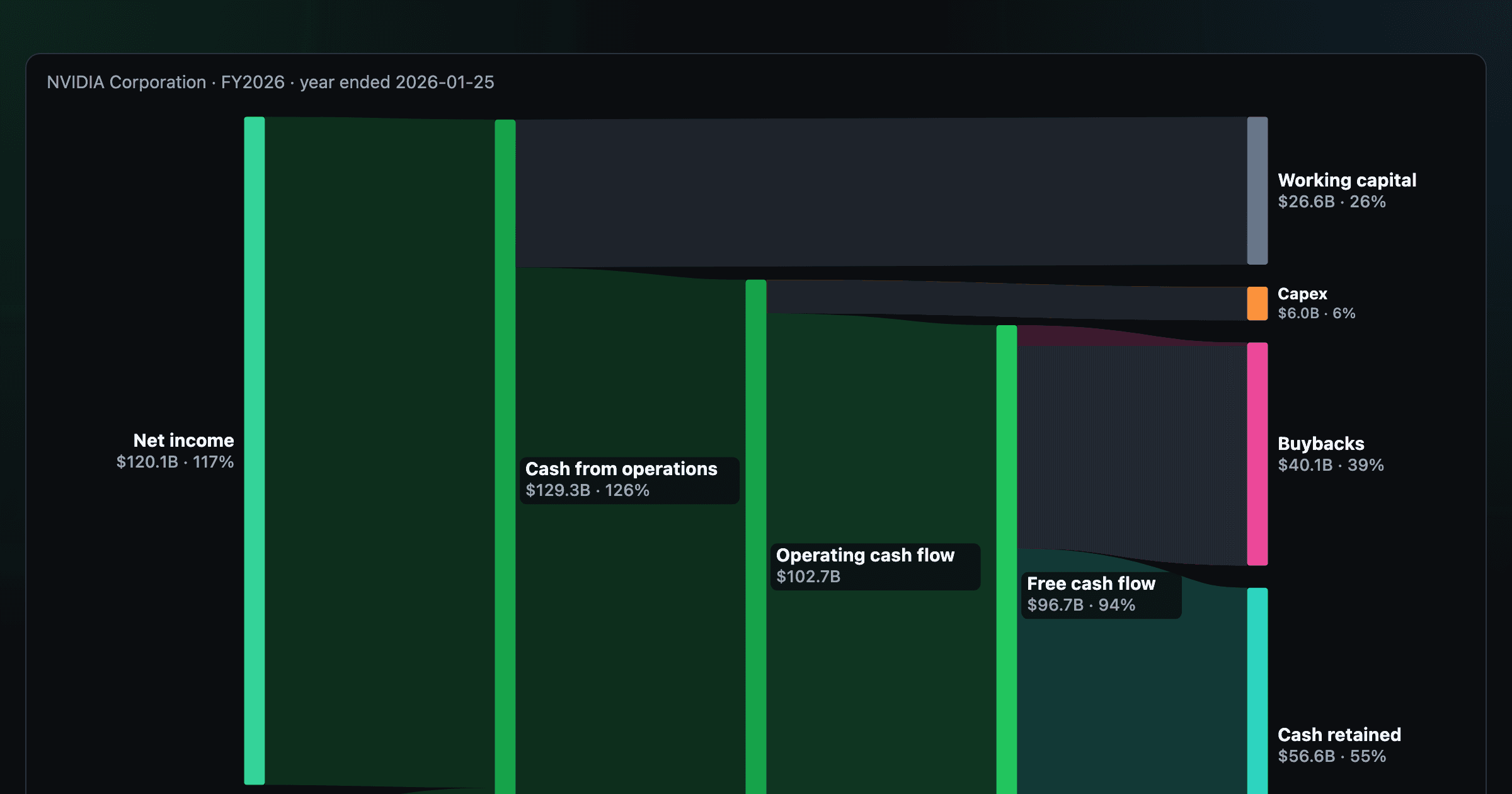

Follow a company's cash from net income through operating cash flow into capex, buybacks, and dividends.

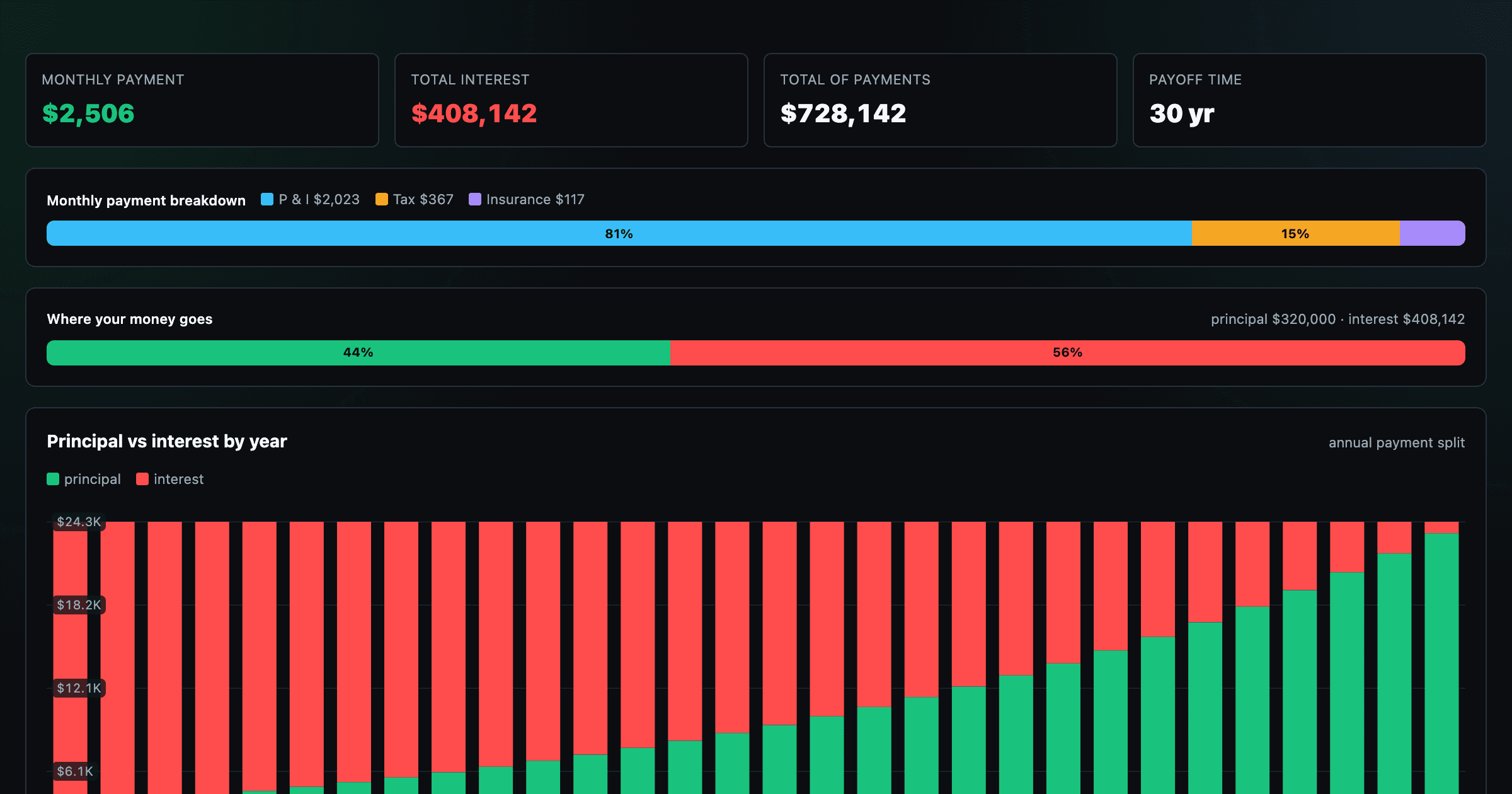

Monthly payment, principal vs interest by year, and the balance paydown — with extra-payment savings.